Based on book: Fundamentals of corporate finance fifth edition (Wiley)

Net working capital = current asset - current liabilities

1. Financial manager and the firm:

Role of the financial manager:

Maximizing the price of firm’s stock will maximize value of a firm and the wealth of its shareholders/owners

3 fundamental decisions in financial management

Capital budgeting: identify which long-term assets to acquire to maximize net benefits for the firm

affect long-term assets (productive assets, tangible or intangible)

Financing: determine best way to pay for for short-term and long-term assets

determine firm’s cpital structure

affect long-term debt and equity thatwill be used to finance firm’s long-term productive asset and net working capital

Working capital: decide how to manage short-term resources and obligations by adjusting current assets and current liabilities to promote growth in cash flow

affect current asset and current liabilities

BOD is representative of all shareholders

mostly large shareholders

sometimes independent experts

Consists of:

audit comittee

governance comittee

remuneration committee: manage composation and performance policies

Financial markets include markets for trading financial assets such as stocks and bonds rather than real assets

Financial institutions include banks, credit unions, insurance companies, and finance companies

Financial system at work

Money is collected from small amounts (borrowed) and invested in large amounts (loaned)

System directs money to the best investment opportunities in the economy (return and risk)

→ Lenders earn profit from lending and borrowing spread

How funds flow through the financial system

Directly vs Indirectly:

Directly through financial markets: creation and sale of financial securities directly to leader/saver

borrower/spedner deals with lender/savers

Investment Bank and money center banks help with origination, underwriting and distribution of new debt and equity

Origination is the process of preparing a security issues for sale

Underwriting is a service to assist firms in selling their debt or equity securities in a direct financing market

Distribution is the process of marketing and reselling the securities to investors

Indirectly through financial institution: institutions invest in Financial Assets by collect money from lender/saver and make loans in larger amounts to borrower/spender

Primary: Wholesale market where firms’ new securities are issued and sold for the first time

Secondary: Retail market where previously issued securities are resold (traded)

enable investors to buy and sell securities frequently

active secondary markets → higher price in primary market

→ companies whose securities have active secondary markets enjoy lower funding costs than similar firms whose securities do not have active secondary markets.

no new money goes into the firm when a secondary market transaction takes place.

Marketability is the ease with which a security can be sold and converted into cash. A security’s marketability depends in part on the costs of trading and searching for information, so-called transaction costs

Liquidity is the ability to convert an asset into cash quickly without loss of value

Broker vs Dealer:

Broker bring buys and sellers together and learn commission fee

Dealers buy from sellers, store to inventory and sell to buyers

Exchanges and over-the-counter markets

Exchange: location where sellers and buyers meet to conduct transactions

New York Stock Exchange (NYSE)

Chicago Board Options Exchange (CBOE)

Over-the-Counter Market: dealers conduct transactions over the phone or via computer

National Association of Securities Dealers Automated Quotations (NASDAQ)

Money and capital markets

Money market: market for low-risk securities with maturities of less than one year

Treasury bills (T-Bills), Commercial paper

Capital market: market for securities with maturities longer than one year

Bonds, Common stock

Capital market are less marketable, higher defauft risk and have longer maturities

Public and private markets

Public markets are organized financial markets where the general public buys and sells securities through their stockbrokers

Private markets involve direct transactions between two parties, often called private placements

Advantages: faster, lower transaction costs

Disadvantages:

Privately placed securities cannot legally be sold in the public markets because they lack SEC registration

Dollar amounts that can be raised tend to be smaller

Futures and options markets

Derivative securities derive their value from some underlying asset

Futures Contract: contracts for the future delivery of assets such as securities, foreign currencies, interest cash flows, or commodities

Options Contract call for the option writer to buy or sell an asset if called upon to do so by the option buyer

Both futures and options can be used to hedge risk

Efficient market hypothesis a theory concerning the extent to which information is reflected in security prices and how information gets incorporated into security prices

Strong-Form Efficiency

Security prices reflect all information, both public and private

Even inside information is reflected in prices

Semistrong-Form Efficiency

Security prices always reflect all public information

Inside, or confidential information, is not reflected in prices

Weak-Form Efficiency

Security prices only reflect historical information

amortization describes the way in which the principal (the amount borrowed) is repaid over the life of a loan.

amortization schedule a table that shows the loan balance at the beginning and end of each period, the payment made during that period, and how much of that payment represents interest and how much represents repayment of principal

With an amortizing loan, some portion of each loan payment goes to paying down the principal

Columns:

Year

Beginning principal balance (1), last year’s Ending Principal Balance

Total monthly/annual payment (2), same every period (CF)

Interest payment (3)

Principal paid (2) - (3) - (4)

Ending Principal Balance (1) - (4) - (5)

Finding interest rate: must use trial and error or calculator

Future value of an Annuity

Future value of an annuity computations typically involve some type of saving activity, such as a monthly savings plan

Another application is computing future values for retirement or pension plans with constant contributions

Given that FVAn=PVAn×(1+i)n, substituting PVA

FVAn=iCF×[1−(1+i)n1]×(1+i)n

FVAn=iCF×[(1+i)n−1]

FVAn=CF×[i(1+i)n−1]=CF×FV annuity factor

Annuities due:

an annuity in which payments are made at the beginning of each period

The present or future value of an annuity due is always higher than that of an ordinary annuity that is otherwise identical

the first cash flow occurs at the beginning of the first period

Annuity transformation method:

Annuity due value=Ordinary annuity value×(1+i)

Level cash flows: perpetuities:

A perpetuity is a series of equally spaced and level cash flows that goes on forever

The most important perpetuities in the securities markets today are preferred stock issues

Perpetuities:

A stream of equal cash flows that goes on forever

Equation for the present value of a perpetuity can be derived from the present value of an annuity equation

PVP=iCF if cash flow is at the end of the first period

Cash flows that grow at a constant rate

Growing annuity

Equally-spaced cash flows that increase in size at a constant rate for a finite number of periods

PVAn=i−gCFi×[1−(1+i1+g)n] where CFi is cash flow one period in the future (CF0∗(1+i%))

only when the growth rate is less than the discount rate

Growing perpetuity:

Equally-spaced cash flows that increase in size at a constant rate forever

PVP=i−gCFi where CFi is cash flow one period in the future (CF0∗(1+i%))

The affective annual interest rate

Annual Percenrage Rate, APR: periodic rate × nb of periods

effective annual interest rate, EAR: annual interest rate that takes compounding over the course of a year into account

EAR = (1+mAPR)m−1

The Appropriate Interest Rate Factor: any time you do a future value or present value calculation, either use the interest rate per period (quoted rate/m) or the EAR as the interest rate factor

8. Bond valuation and structure of interest rate

Corporate bonds

Market for corporate bonds

The most important investors are life insurance companies, pension funds, and mutual funds

Transactions tend to be in very large dollar amounts

less efficient compared to stocks or U.S. treasury bills and bond

Bond price information:

Only a small fraction of the bonds outstanding are traded each day

Mostly negotiated directly between the buyer and seller, with limited centralized reporting of the sales

Corporate bond:

A type of Fixed-income securities: debt instruments that pay interest in amounts that are fixed for the life of the contract

Features of corporate Bonds:

Long-term claims against company assets

Face, or par, value is $1,000

Coupon rate is the annual coupon payment (C) / bond’s face value (F)

Coupon payment is a fixed amount paid to lenders for the life of the contract (typically with a semiannual or annual payment)

Types of corporate bonds:

Vanilla bonds, debentures, are unsecured:

Coupon payments fixed for the life of the bond

Repay principal and retire the bonds at maturity

Contracts have the features and provisions found in most bond covenants

Annual or semiannual coupon payments

Zero coupon bond:

No coupon payment, only face value at maturity

Sold at a discount compared to face value

Convertible bonds:

May be exchanged for shares of the firm’s stock

Sell for a higher price than a comparable non- convertible bond

Bondholders benefit if the market value of the company’s stock gets high enough

Bond valuation

Steps:

estimate the expected future cash flows

determine the required yield, rate of return, or discount rate (depends on riskiness of the future cash flows)

market interest rate

compute present alue of future cash flows

Bond valuation formula:

Then PB (current value/price of a bond = PV (present value of coupon payments) + PV (present value of Principal payment)

PB=(1+i)C1+(1+i)2C2+...+(1+i)nCn+Fn

Par, premium and discount bonds

Par bond: If a bond’s coupon rate is equal to its yield, the price will equal the face value

Premium bond: If a bond’s coupon rate is more than its yield, the price will be higher than the face value

Likely to happen when interest rates are falling

Discount bond:

If a bond’s coupon rate is less than its yield, the price will be less than the face value

Likely to happen when interest rates are rising

Semiannual compounding:

i=i/m

C=C/m

Zero coupon bonds: discount simply

PB=(1+i/m)mnFmn

Bond yields:

YTM, Yield to maturity:

actual rate of return (if buy bond now) != interest rate (used to calculate what bond price should be)

EAY, Effective annual yield:

EAY=(1+mquoted interested rate)m−1

quoted interested rate = nb of periods * YTM

Realized Yield: return earned on a bond given cash flow actually received

Interest rate risk

uncertainty about future bond values due to the unpredictability of interest rates

Bond theorems:

Bond prices are inversely related to interest rate movements

interest rate increase → more discount → cheaper present value

For a given change in interest rates, prices on longer-term bonds change more than prices of shorter-term bonds

longer-term bond’s present value discount much more or much less compared to shot-term bond

For a given change in interest rates, prices of lower-coupon bonds change more than prices of higher-coupon bonds

more capital concentrate at longer period discounts

→long term, zero coupon is most sentitive

Bond theorem application: if interest rates are expected to increase, avoid long-term bonds

If interest rates are expected to decrease, buy zero-coupon bonds

Call provision: allow bond issuer to purchase a bond from bondholder at a pretermined price before maturity

more likely to be called when interest rates decline

CIP, call premium, =icallable−inon-callable>0

Default risk: borrow might not pay back interest and or principal

DRP, default risk premium, =idr−irf>0

interest for default risk - interest for risk-free rate

Bond ratings: rank bonds in order of probability of default

Investment grade / noninvestment grade

State and federal laws typically require commercial banks, insurance companies, pension funds, certain other financial companies, and government agencies to purchase only investment-grade securities

The term structure of interest rate

refers to the relationship between yield to maturity and term-to-maturity on a bond

Yield curve:

Ascending or normal yield curves slope upward from left to right and imply higher interest rates are likely

Descending or inverted yield curves slope downward from left to right and imply lower interest rates are likely

Flat yield curves imply interest rates are unlikely to change

Factors that shape the yield curve:

Real rate of interest

Expected rate of inflation:

if higher inflation is forecast, the YC slope upward because longer-term yields will contain larger inflation premium than shorter-term yields

interest rate risk

The longer the maturity of a security, the greater its interest rate risk (the risk of selling the security at a lower price) and the higher the YTM

The interest rate risk premium adds upward bias to the slope of the yield curve

Cumulative effect of factors that shape the yield curve:

In an economic expansion

The real rate of interest and inflation premium increase monotonically

Interest rate risk increases

In an economic contraction

The real rate of interest and inflation premium decrease monotonically

Interest rate risk decreases

Yield curve to recession:

expectation: investors expect long-term to have lower interest rate and inflation rate

9. Stock valuation:

Market for stocks:

secondary market

NASDAQ

NYSE

The world’s stock exchange

Efficiency of secondary markets

4 types of secondary market, order from least to most efficient:

Direct search: cost of locating and negoriating

Broker: cost of commission paid to broker who bears the cost

P0=t=1∑∞(1+R)tDt where R is required rate of return

doesnt yet account for selling stock

only for dividend forecasts

doesnt include assumptions:

growth rate is constant

forecasting dividends or when shares are sold

Growth stock pricing paradox

stock of a company whose earnings are growing at an above-average rate and are expected to continue to do so for some time

Rapidly-growing firms

Typically pay no dividends on common stock in the growth phase

Have many high-return investment opportunities, making investors are better off if firms reinvest earnings

shares of a company that will never pay cash to investors are worthless

In reality, high-growth firms will eventually pay dividends

If investments made with reinvested funds succeed, a firm’s net cash inflows should increase significantly and investors can sell their stock at a much higher price than what they paid

Stock valuation: some simplifying assumptions

These apply for both common stock and preferred stock

Zero-growth dividend model:

P0=RD

Constant growth dividend model:

Dt=D0×(1+g)t

P0=R−gD1 where D1 is dividend in year 1

Computing future stock prices:

Pt=R−gDt+1

Mixed (supernormal) growth dividend model:

If the supernormal growth occurs first and is followed by constant dividend growth, we can combine equations

It can be proven that portfolios with more than one asset is always less risky

Risk can be reduced by creating a portfolio using assets having different risk charatersistics

Limits:

When the number of assets in a portfolio is large, adding another stock has almost no effect on the standard deviation

Most risk-reduction from diversification may be achieved with 15 to 20 assets

Diversification can virtually eliminate risk unique to individual assets, but the risk common to all assets in the market remains

unsystematic or diversifiable: risk that can be eliminated through diversification

systematic or nondiversifiable: risk that cannot be eliminated through diversification

Systematic risk (market risk)

Well-diversified portfolios contain only systematic risk

Competition among diversified investors will drive the prices of assets to the point where the expected returns will compensate investors for only the systematic risk

Measuring systematic risk:

The market’s influence on a stock’s return is quantified in the stock’s beta

If the beta of an asset is:

Zero, the asset has no measurable systematic risk

Greater than one, the systematic risk for the asset is greater than the average for assets in the market

Less than one, the systematic risk for the asset is less than the average for assets in the market

Risk Premium:

Compensation for Bearing Systematic Risk

E(Ri)=Rrf+ Compensation for bearing Systematic riski

returned on risky asset = risky free rate + risk premium

illustrates the CAPM’s prediction for the required expected total return for various values of beta

expected return greater than the required return estimated with the CAPM → the expected return plot above the SML →underpriced

expected return less than the required return estimated with the CAPM → the expected return plot below the SML →overpriced

10. Fundamental of capital budgeting

Introduction:

The Capital Budgeting Process

Starts with the firm’s strategic plan which describes its strategy for the next three to five years

Division managers then convert the firm’s strategic objectives into business plans

The capital budget is generally prepared jointly by the CFO’s staff and financial staff at the divisional and lower levels, reflecting the activities outlined in the divisional business plans

steps:

Idea generation

Investment analysis

capital allocation planning

monitoring and post-audit

Key Reasons for Making Capital Expenditures: ranked from least to most risky

replacement: an asset will have to be replaced rather than repaired or overhauled

an expansion: new equipment to produce more products or expansion of the firm’s distribution system.

new products and services: involve more stakeholders and higher degrees of risk

regulatory, safety and environmental: required by third party, such as the gov or insurance company, to meet specified standards.

Others: such as management pet proejects and high-risk investments which falls outside normal project analyses

Source of information:

generated internally, often beginning with the sales force

Next the production team gets involved, followed by accountants

All the information is reviewed by financial managers who evaluate the feasibility of the project

Classification of investment projects;

Independent projects: accept or reject doesnt influence decision about other projects being considered

when resources are not limited

Mutually exclusive projects: only 1 or the other

Contingent projects: one project depends on on another’s acceptance

Basic capital budgeting terms:

cost of capital: rate of return that a project must earn to be accepted by management

riskier → higher cost of capital

capital rationing: a firm with limited funds choose the best projects to undertake

NPV compares the PV of expected benefits and cash flows from a project tp the PV of expected costs

if benefit > cost, the project is feasible

NPV techniques

NPV = PV of expected inflow - PV of expected cash outlow = Cash inflow - Cash outflow

when NPV = 0, IRR = cost of capital → still profit (atleast beat inflation)

5 steps:

Determine the intial cost of starting the project? next lec

estimate the project’s future cashflows over its expected lift? next lec

find the riskiness of the project and appropriate cost of capital

the risker a project, the higher its cost of capital

compute the project’s NPV

make a decision

Mutually exclusive projects and NPV

managers should allocate capital to the project that has the most positive dollar impact on the value of the firm—in other words, the project with the highest NPV

Key advantage:

use discounted cash flow valuation

provide a direct (dollar) measure of how much capital that project will increase firm’s value

consistent with the goal of maximizing stockholder value

Decision: Payback period ⇐ payback cutoff point → accept

advantages:

easy to calculate and understand

simple measure of a project’s liquidity risk

disadvantages:

Simple payback period doesnt account for TVL

doesnt consider cash flows past payback period

bias against long-term projects

arbitrary cutoff point

Internal Rate of Return (IRR)

Definition:

The discount rate which a firm’s cost of capital to the rate-of-return that makes the net cash flows from a project equal its cost

discount rate that makes NPV = 0

Calculating IRR: with trial and error method

When IRR and NPV agree?

evaluating independent projects

projects’ cashflows are conventional, ones with intial cash outflow followed with cash one or more inflows

When IRR and NPV disagree?

unconvential cash flows → might have multiple IRR

mutually exclusive project

→ always go for NPV

IRR for mutually exclusive projects:

a discount rate at which the NPVs of two mutually exclusive projects will be equal

that rate is the crossover point

Depending on whether the required rate of return is higher or lower than the crossover rate, the ranking of the projects will be different

It is easy to identify the superior project based on NPV, but it cannot be done using IRR due to ranking conflicts

→ if cost of capital < crossover rate: take project A

IRR vs NPV:

IRR assumes that cash flows from a project are reinvested to earn with the rate of IRR while NPV assumes that it will earn the firm’s cost of capital

explain for IRR: for example, positive cashflow at somewhere in the middle is discounted forward, that means it is assumed to be reinvested at same rate

optimistic assumption in the IRR method leads to some projects being accepted when they should not

because the reinvested cash flows cannot earn the IRR

Summary for IRR:

if IRR > cost of capital → accept

advantages:

intuitive and easy to understand

based on discounted cash flow technique

disadvantages:

With nonconventional cash flows, IRR approach can yield no usable answer or multiple answers

A lower IRR can be better if a cash inflow is followed by cash outflows

With mutually exclusive projects, IRR can lead to incorrect investment decisions

IRR calculation assumes cash flows are reinvested at the IRR

Modified IRR (MIRR)

IRR is too optimistic → MIRR assumes the cash flow to be reinvested at firm’s cost of capital

TV = Sum of FV value

MIRR is the rate for which PVcost=(1+MIRR)nTV

Investment Decisions with Capital Rationing

Capital rationing in a single period

Profitability Index (PI) provides a measure of the value of project generates for each dollar invested in that project

Useful for capital rationing when firms have limited resources and therefore cannot invest in all projects that have a positive NPV

Consistent with the idea of shareholder wealth maximization

Practitioners’ Methods of Choice: IRR is currently popular

Postaudit and Periodic Reviews:

Management should systematically review the status of all ongoing capital projects and perform post-audits on completed capital projects

A review should challenge the business plan, including cash flow projections, cost assumptions, and the performance of people responsible for implementing the capital project

A post-audit examination may reveal why a project was successful or failed to achieve its financial goals

11. Cash flows and capital budgeting

Calculating project cash flows:

Capital allocation assumptions:

Decisions are based on cash flows (not net income/op income which are done in (Accrual Basis Accounting)

Cash flows are not accounting net income or operating income

Cash flows are based on opportunity costs

Cash flows are analyzed on after-tax basis

Timing of cash flows is crucial

Financing costs are ignore

Incremental after-tax free cash flows (FCF):

the total after-tax free cash flows the firm would produce with the project, less the total after-tax free cash flows the firm would produce without the project

FCFproject=FCFfirm with project−FCFfirm without project

left-hand side: total market value of assets, the present value of total cash flows that those assets are expected to generate in the future

value of investors’s claims must be equal to value of cash flows they have a right to receive

total market value of the debt and equity of a firm is the present value of the cash flows that the debt holders and stockholders have the right to receive

MV of Assets = MV Current Assets + MV of PPE + MV other asset = MV of Liabilities + MV of Equity

The overall cost of capital structure is what it costs the company to raise additional capital using the specified mixture of debt and equity

Importance of cost of capital:

basis of appraising new capital expenditure proposals

recommended risk-free rate is the rate on long-term treasury security

beta can be estimatd with regression analysis, but much more complicated if common stock is not publicly traded

market risk premium is not possible to be observed, analysts generally use a measure of avg risk premium investors have actually earned as an indicator

constant growth divident model: solve for required rate of return

P0=R−gD1

→kcs=P0D1+g

must estimte the dividend that stockholders will receive in next period, D1 as well as rate ,g, that the market expect in long term

multistage-growth dividend model: solve for required rate of return

Preferred stock

Characteristics of prefered stock allow us to use the perpetuity model to estimate cost of preferred equity

P0=RD→kps=PpsDps

Using the WACC in practice

Limitations of WACC as a Discount Rate for Evaluating Projects

financial theory tells us that rate should be used to discount these incremental cash flows is the rate that reflects their systematic risk

→ WACC is going to the appropriate discount rate for evaluating a project only when the project has cash flows with systematic risks that are exactly the same as those for the firm as a whole

WACC = xdebtkdebt-pretax(1−t)+xpskps+xcskcs

should use market values rather than book values

donot include retained earning

conditions for using the WACC:

Alternatives to using WACC:

14. Working capital management

Working capital basics

Involves 2 key issues:

what is the appropriate amount and mix of current assets to hold

how should these current assets be financed

Terms and concept:

current assets: cash and other assets that the firm can convert into cash in a year or less

current liabilities: obligations that the firm expects to pay off in a year or less

working capital: funds invested in a company’s cash account, account receivables, inventory, and other current assets

NWC: current assets - current liabilities

working capital efficiency: length of time between when a working capital asset is acquired and when its converted into cash

liquidity: ability of a company to convert real or financial assets into cash quickly and without loss of value

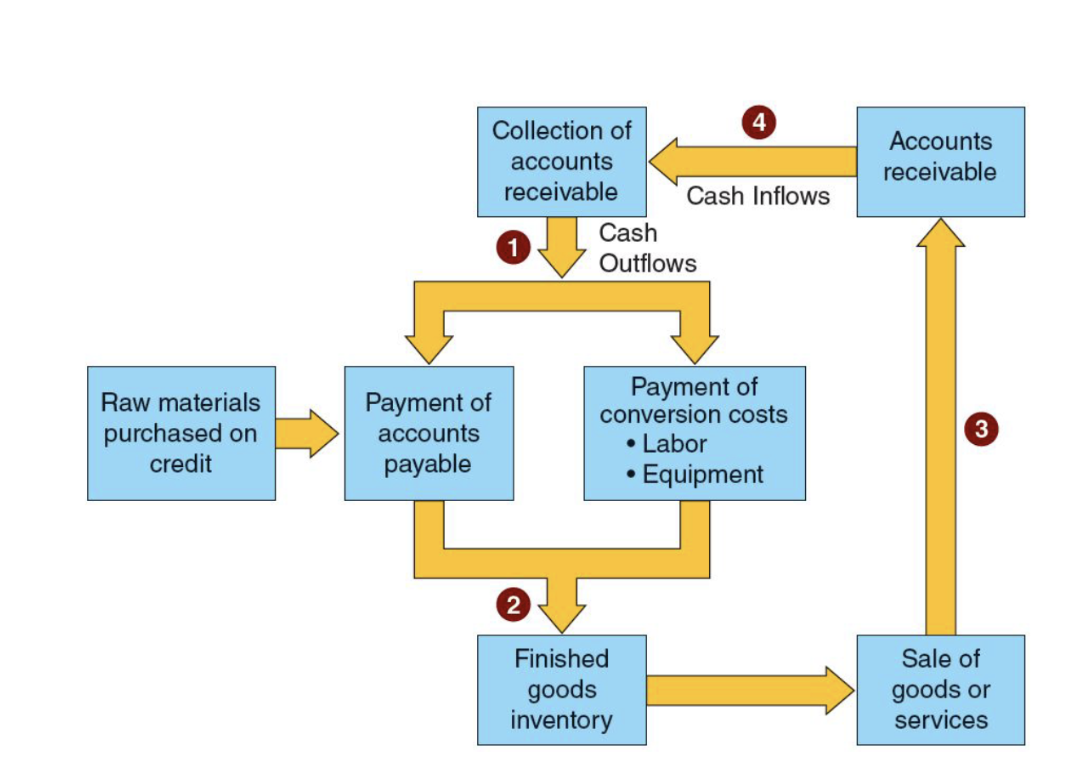

The operating and cash conversion cycles

Cash conversion cycle: the point a company pays for raw materials until the point it receives cash from sales

Sequence of events:

use cash to pay for raw materials and costs of conversion

finished goods are hold in inventory

finished goods are sold on credit

customers repay credit

Cash conversion cycle:

Goals of financial managers:

delay paying accounts

maintain minimum raw material inventories

to use as little labor as possible

maintain minimal finished goods in inventories

offer customers the most attractice credit terms

collect cash payments as fast as possible

Operating cycle:

begins when cash is used to purchase raw materials and ends when cash is collected (debit or credit)

=DSI+DSO

Cash Conversion Cycle

starts when the firm actually pays for inventory until when cash is received

can be negative

=DSI+DSO−DPO=Operating cycle−DPO

Days’ Sales in Inventory (DSI) shows how long the firm keeps its inventory before selling it

→ if cost of capital < crossover rate: take project A